Best Practices for Businesses to Detect the Business Email Compromise Scam

For a comprehensive list of strategies for detecting and preventing the BEC scam, download the guide and share it with all employees.

By clicking this link you are now leaving parkbankonline.com and entering a third party website. Park Bank is not responsible for any of the content, links, privacy policy or security policy of this website.

What happens if an employee follows through on sending the wire?

Chances are you will never see your money again. The transferred money is usually liquidated immediately after the wire is received on the other end.

Why this scam works?

Employees have busy schedules and are eager to please their boss or a member of senior management without challenging the unusual nature of the request.

Key takeaway:

Ask: Does the request appear reasonable? Is there a sense of urgency to the request? Does the writing style appear awkward?

Authenticate: Email addresses can be spoofed or breached. Know who you are communicating with.

Approve: Have a written procedure in place for approving outgoing wire requests. It's okay to ask questions.

Cybercriminals are attacking businesses in our area with a twist to the old-fashioned email scam. They’ve discovered the effectiveness of target marketing and personalization. Nationally, the FBI reports that over 8,000 companies have lost an average of $150,000 per incident.

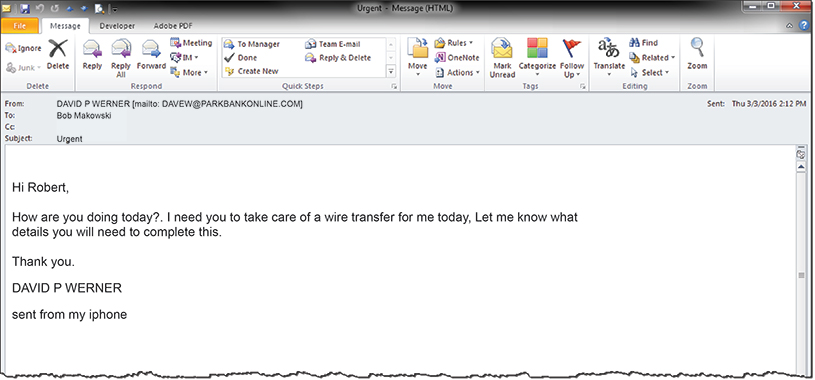

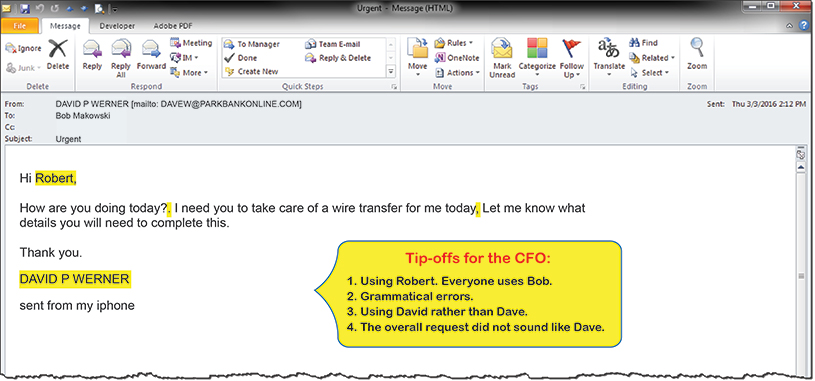

Called the Business Email Compromise (BEC) scam, it starts with a message that appears to be sent from a company’s CEO or CFO to trick employees into wiring money to fraudsters. No business is immune from being targeted, including a bank. In fact, our CFO continues to receive fraudulent emails. We have replicated one of the requests below:

We have seen other fraudulent emails contain all of the specifics of the wire transfer – the beneficiary, the account number, the amount and the ABA number so that the targeted employee had all the information they needed to send the wire without having to verify any information. In our case, our CFO was tipped off to the fake email based on multiple factors.

Cyber insurance does not necessarily cover losses due to the business email compromise because of an exclusion clause stating there is no coverage for “voluntary parting”, even if the employee was duped. To understand your policy or to inquire about cyber insurance, check with your insurance agent. Source: Bank Investment Daily, www.pcbb.com

This article has been prepared for general informational purposes only and is not intended to be relied upon as professional advice. It is presented without any representation or warranty as to the completeness of the information.